US large cap stocks as represented by the S&P 500 index currently has a 26x Shiller P/E vs. its historic median of 16x. In terms of the Shiller P/E measure the S&P 500 index valuation is stretched. US small cap stocks as represented by the Russel 2000 index currently has a 46x Shiller P/E vs. its historic median of 40x. In terms of the Shiller P/E measure the Russel 2000 index valuation is close to its historic median.

US large and small cap stocks current Shiller P/E vs historic median:

Source: Research Affiliates LLC.

First of all, do not pay too much attention to the net of inflation expected return calculated by Research Affiliates Inc. as the expected return is based on the reversion of the Shiller P/E measure and a 10 year forecast of both economic growth and dividend growth. Do not fully trust 10 year forecasts as the future is more random than what analysts are willing to admit.

Although US large cap stocks as represented by the S&P 500 looks expensive from a Shille P/E standpoint one may argue that the current pricing is in equilibrium:

- The recent S&P 500 correction has slightly improved the index Shiller P/E

- The forward S&P 500 P/E multiple is currently close to its 20 year average

- The index data dates back as far as 1871. One may wonder if 19th century asset pricing is relevant today. I am quite sure that the current S&P 500 Shiller P/E would look less stretched if compared to the last 25 years median

- Current risk-free interest rates are low. If you remember CAPM from school such low rates support higher valuation multiples as low interest rates decrease the discount rate applied to future cash-flows in DCF valuations

- The S&P 500 index is less volatile than many other comparable international indexes

- Compared to its historic median the S&P 500´s Shiller P/E is skewed as the measure includes depressed financial crisis earnings

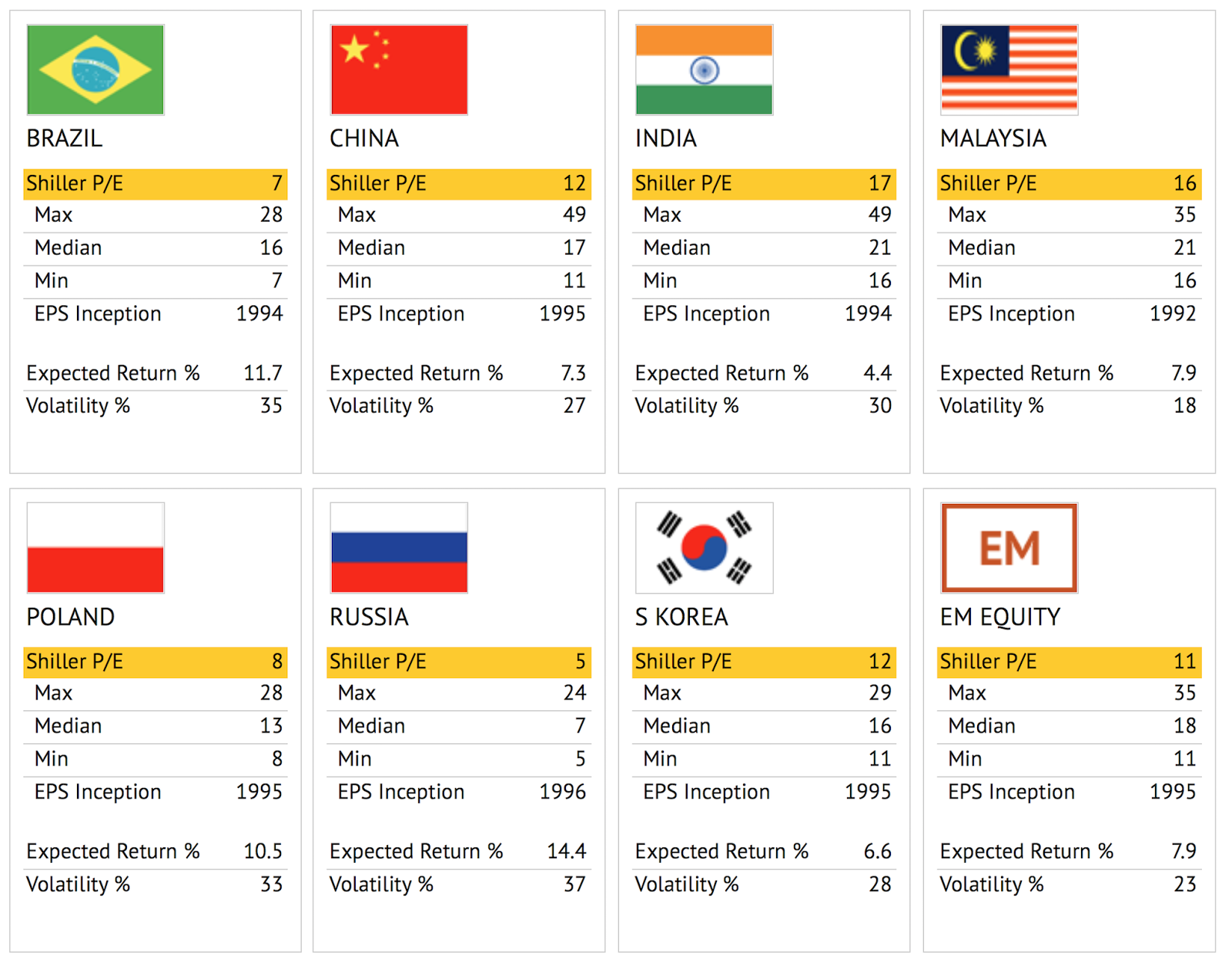

As an alternative to US stocks you may want to take a look at the below mentioned emerging markets which currently are priced at or close to the minimum of their historic Shiller P/E ranges. Note that the data is based on USD inputs. Keep in mind that some of these Shiller P/E´s are supported by shorter data time-series, resulting in less reliable Shiller P/E measures. Furthermore some of these markets are changing rapidly which may result in an even less reliable Shiller P/E measures. Some of these economies are currently in trouble and you need to be a believer in cyclical rebounds in order to find them investable. However if you are a contrarian like I am you should definitely take a second look at these:

Selected emerging markets Shiller P/E vs historic median:

- Brazil is represented by: MSCI Brazil index

- China is represented by: MSCI China index

- India is represented by: MSCI India index

- Malaysia is represented by: MSCI Malaysia index

- Poland is represented by: MSCI Poland index

- Russia is represented by: MSCI Russia index

- South Korea is represented by: MSCI South Korea index

- EM Equity is represented by: MSCI Emerging Markets index

Disclosure: I am long MSCI Emerging Markets UCITS ETF (acc).

I wrote this article myself, and it expresses my own opinions. I am not receiving any compensation for it.